To be perfectly honest, I thought the above was true - until I decided to delve deeper to see what was going to happen to my family's tax bill.

Remember the old saying "The Devil is in the details"? Well, let me introduce you to a little devil called the Recapture Rule! (I swear I didn't make this up).

Ok, stay with me. The local municipalities calculate your property's worth 3 ways:

- Just/Market Value - a market value assigned by the taxing authority

- Assessed Value - the value of the property assigned for tax value (usually less than Just/Market Value)

- Taxable Assessed Value - after exemptions, the amount you, the owner, are taxed on.

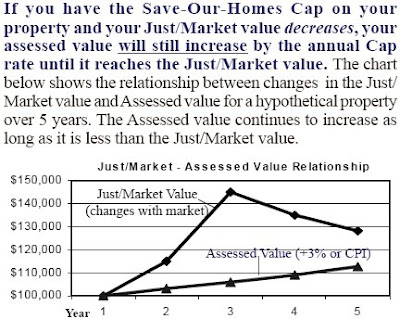

For most homeowners, their Just/Market Value will be higher than their Assessed Value. If they have Homestead, then the max their Assessed Value can increase on a yearly basis is 3% (or the CPI).

So let's say your Just/Market Value is $200,000 and your Assessed Value is $150,000. Next August when you receive your TRIM notice, you will see a decrease in your tax bill because your Just/Martket Value will be less than $200,000, right? WRONG. Please read the snippet below that is taken directly from the Pinellas County Property Appraiser website, http://www.pcpao.org/:

Details, meet Devil. Devil, meet Details.

Details, meet Devil. Devil, meet Details.

Keep on keeping on!

No comments:

Post a Comment